Introduction:

Volatility is a crucial concept in the world of options trading. It refers to the degree of price fluctuations a financial instrument experiences over a specific period. As an options trader, understanding volatility is essential for making informed decisions and managing risk effectively. In this article, we will delve into the significance of volatility in options trading and explore how it influences option prices and strategies.

Volatility and Option Prices:

Volatility plays a significant role in determining the price of options. Higher volatility typically leads to higher option premiums, while lower volatility results in lower premiums. This is because increased volatility implies a higher likelihood of significant price swings, making options potentially more valuable to traders.

Implied Volatility (IV):

Implied Volatility (IV) is a forward-looking measure of volatility, representing the market’s expectations for future price movements. It is a crucial component of option pricing models, such as the Black-Scholes model. Traders use IV to assess whether options are relatively cheap or expensive compared to historical volatility. In options trading, implied volatility is far more important than historical volatility.

Historical Volatility (HV):

Historical Volatility (HV) calculates past price fluctuations to gauge how volatile an underlying asset has been over a specific period. By analyzing HV, traders can gain insights into the stock’s past behavior, helping them make more informed predictions about future volatility. Historical volatility is less important than implied volatility for traders looking to make an options trade. This is because one looks backwards and one looks forwards.

Volatility Skew:

Volatility skew refers to the unequal implied volatilities among options with different strike prices but the same expiration date. It often occurs when options traders perceive varying levels of risk for different price levels of the underlying asset. The presence of volatility skew can influence trading decisions and option strategies.

Volatility Index (VIX):

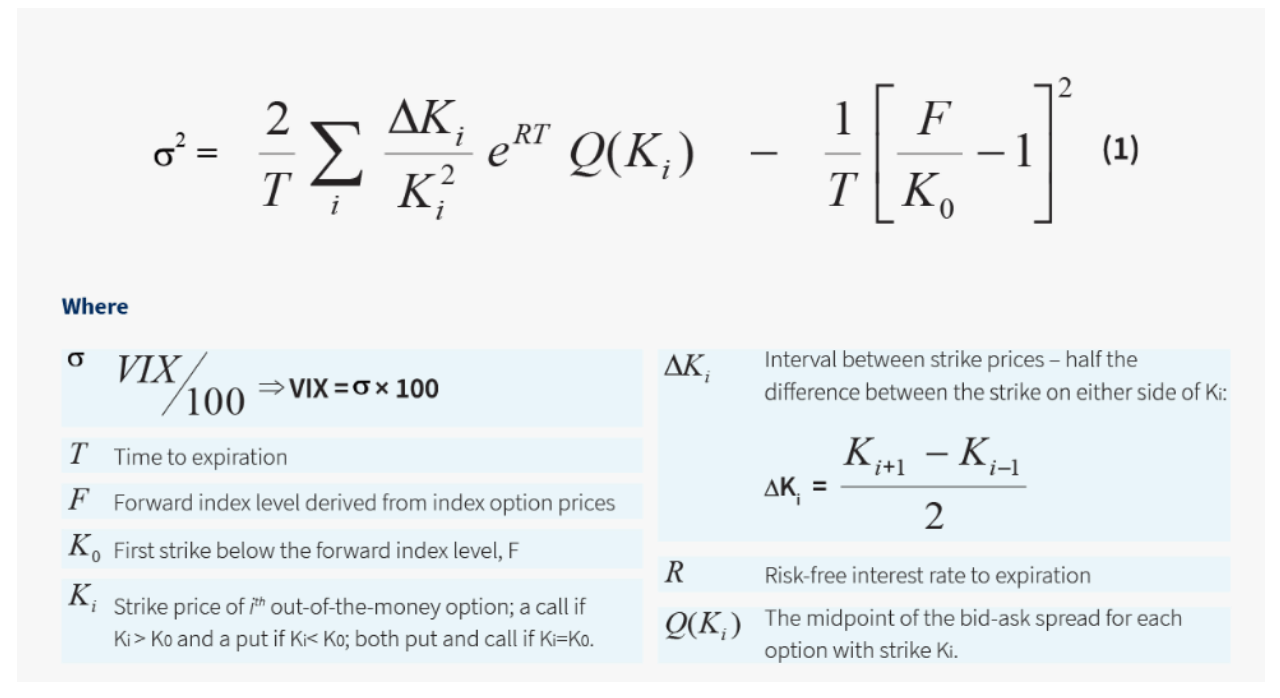

The Volatility Index, commonly known as VIX or the “fear gauge,” measures the market’s expectations of future volatility. It represents the market’s sentiment and provides insights into investor perceptions of risk. High VIX levels indicate increased market uncertainty, while low VIX levels suggest a calmer market. The VIX is calculated using out of the money puts and calls on the SPX using the following simple (sarcasm) formula courtesy of cboe.com

Volatility-Based Strategies:

Options traders employ various volatility-based strategies, such as straddles, strangles, and iron condors. These strategies aim to profit from expected increases or decreases in volatility. Volatility-based strategies can be effective around events like earnings announcements or major economic releases. The general rule of thumb is that volatility will be very elevated coming into the event and will collapse immediately after. In that sense, the phrase “buy on the rumor, sell on the news” is very applicable to volatility.

Conclusion:

Volatility is a critical aspect of options trading that significantly influences option prices and strategies. Understanding both implied and historical volatility helps traders assess option pricing and market sentiment accurately. Additionally, volatility skew and the Volatility Index provide valuable insights for crafting effective trading strategies. By incorporating volatility considerations into their trading decisions, options traders can navigate the market with greater confidence and efficiency.